The launch of the Goods and Services Tax Appellate Tribunal (GSTAT) on 24th September 2025 marks a historic milestone in India’s GST journey. For the first time, taxpayers now have a single, independent national forum to resolve GST disputes beyond the first appellate stage.

To help businesses, professionals, and entrepreneurs understand this change better, we’ve prepared a simple FAQ. The answers are concise, practical, and business-friendly — so you can focus on what matters most: running your business with confidence.

FAQ

Q1 : What is the GST Appellate Tribunal (GSTAT) and why was it launched?

Answer:

The GST Appellate Tribunal (GSTAT) is a new statutory appellate body under the GST law, set up to hear second-level appeals against orders of GST appellate authorities (the first appeal level).

It was officially launched on 24 September 2025 by the Union Finance Minister, with the goal of providing an independent, national forum for taxpayers to seek justice in GST disputes. The GSTAT is meant to deliver swift and fair resolution of GST disagreements, reducing the burden of prolonged litigation on businesses.

It represents an evolution of the GST system to “One Nation, One Forum for Fairness and Certainty”, ensuring that whether an original order was passed by a central or state authority, the next appeal now goes to a single, unified tribunal.

The government launched GSTAT to strengthen trust in the tax system and improve ease of doing business.

Key reasons for establishing GSTAT include:

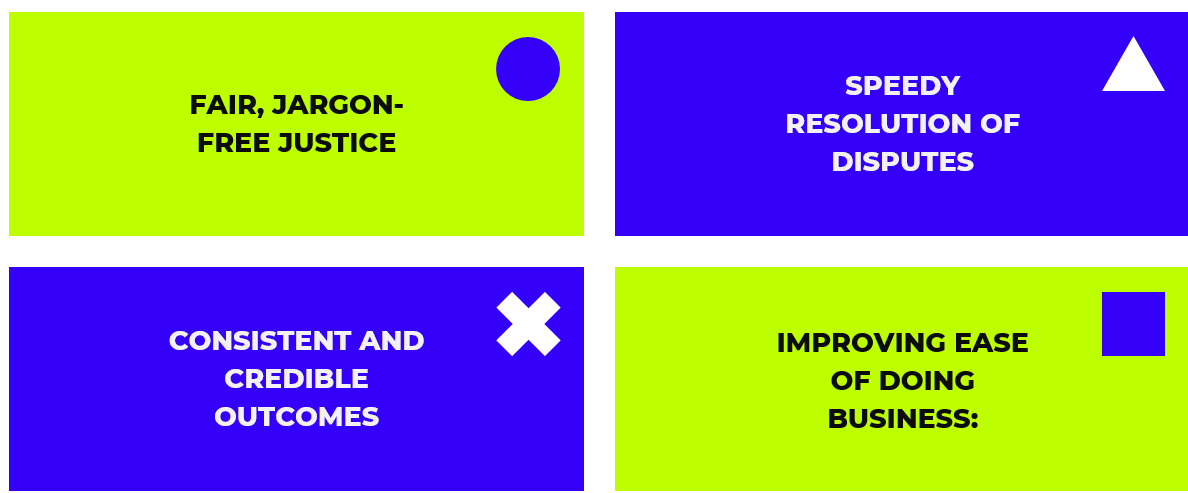

- Fair, Jargon-Free Justice:

The tribunal is expected to issue clear, jargon-free decisions in plain language, using simplified formats and checklists, so that taxpayers can understand outcomes easily. It adopts digital-by-default processes (online filings and even virtual hearings) to make dispute resolution user-friendly and transparent from day one. - Speedy Resolution of Disputes:

GSTAT is tasked with adhering to strict timelines for listing, hearing, and pronouncement of orders, so that disputes do not linger. The aim is “no delay in justice” – every taxpayer’s appeal should be heard promptly and decided without undue wait. This helps businesses avoid cash flow issues caused by long-pending tax cases. - Consistent and Credible Outcomes:

As a national tribunal with benches across India, GSTAT will bring consistency in interpretation of GST laws and predictability in outcomes. A dedicated appellate forum boosts confidence that decisions will be impartial and consistent nationwide, instilling trust among taxpayers. - Improving Ease of Doing Business:

By reducing legal friction and addressing disputes efficiently, GSTAT makes the GST system more reliable and business-friendly. It is seen as a “vital forum for justice” and a natural extension of GST reforms to ensure the tax system remains fair, transparent, and conducive to investment.

In summary, GSTAT has been launched to ensure that GST is not only a “Good and Simple Tax” but also a fair and trustworthy tax regime where businesses of all sizes can resolve their tax issues swiftly and focus on growth.

Q2 : Who can file an appeal to the GST Appellate Tribunal, and under what conditions?

Answer:

Any person or business aggrieved by the decision of a GST first appellate authority or a revisional authority can file an appeal with the GST Appellate Tribunal (under Section 112 of the CGST Act). In practical terms, this means if you have received an order in Form GST APL-04 (order from the first appellate authority, usually the Commissioner (Appeals)) or an adverse decision in a revisional proceeding (Form GST RVN-01), you have the right to approach the GSTAT for a second appeal.

Here are the conditions and requirements for filing an appeal to GSTAT:

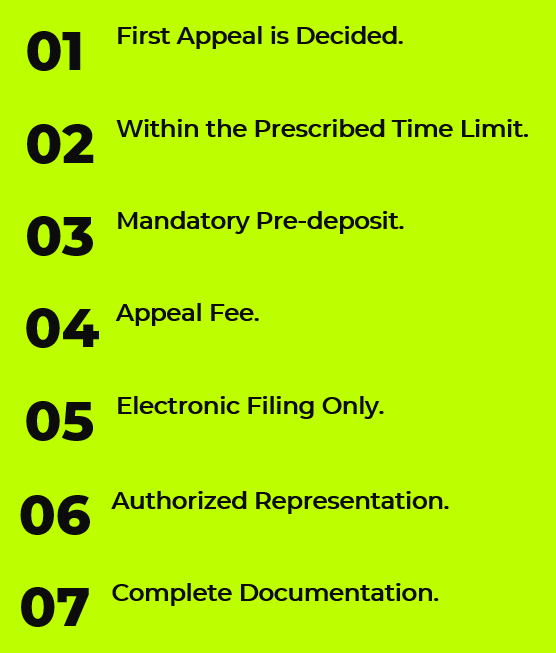

- First Appeal is Decided:

You can appeal to GSTAT only after getting the decision from the first appellate stage (or a revision order by a Commissioner). The GSTAT will review those orders passed by appellate authorities or revisional authorities under Sections 107 and 108 of the GST Act . (You cannot skip the first appeal and directly go to the tribunal in normal circumstances.) - Within the Prescribed Time Limit:

Appeals to GSTAT should be filed within the allowed time frame.

Special Extension: Since GSTAT is newly operational, there is a one-time extended window (up to 30 June 2026) with staggered deadlines for older cases (see the next FAQ). Going forward (for orders communicated on or after April 1, 2026), appeals must be filed within the standard 3 months from the date of the first appellate order. It’s important to adhere to these timelines to ensure your appeal is admitted. - Mandatory Pre-deposit:

A stipulated pre-deposit of the disputed tax/penalty amount is required before filing the appeal, as per Section 112(8) of the CGST Act. In essence, you must pay a percentage of the contested amount (after adjusting what’s already paid at the first appeal stage) as security. This pre-deposit is to be paid into the government treasury and proof of payment must be provided. The GSTAT portal will prompt you for details of this payment (often referred to as “pre-deposit” ) during the filing process. Ensure this amount is paid – otherwise the appeal cannot be admitted. (This requirement is similar to the first appeal stage where 10% of the tax in dispute is paid; an additional amount is required for the tribunal appeal, making total 20% in many cases.) - Appeal Fee:

Apart from the pre-deposit, a nominal court fee/appeal fee has to be paid for filing the appeal. The GSTAT e-filing portal integrates with Bharatkosh (the government payment gateway) to collect this fee online. You can pay via net banking, card, UPI etc., and a challan/receipt will be generated. If you pay the fee offline on Bharatkosh, you’ll need to upload the challan as proof. - Electronic Filing Only:

All GSTAT appeals must be filed electronically on the official GSTAT e-filing portal (https://efiling.gstat.gov.in). The tribunal does not accept paper or offline filings. Both the appeal application and all supporting documents should be submitted online through this system as per the GSTAT (Procedure) Rules, 2025. Hearings may also be conducted virtually via this portal’s e-court system for convenience. - Authorized Representation:

You can file the appeal yourself or through an authorized representative (such as a tax professional, CA, lawyer, or company executive). The GSTAT portal allows you to add your representative’s details in the appeal form. If you appoint a representative, a Vakalatnama (power of attorney/authorization letter) will need to be uploaded to authorize that person. Ensure your representative is registered on the GSTAT portal (there is a separate registration for authorized representatives) so that you can select their name while filing. - Complete Documentation:

Conditions for a successful filing include uploading all required documents: the appeal memorandum (grounds of appeal), a copy of the impugned order (the order you are appealing against), any supporting evidence or annexures, and the authorization letter (Vakalatnama) if applicable. All documents must be in PDF format and under the size limit (each file up to 20 MB). Having these documents ready will smoothen your online filing process.

In summary, any taxpayer (or even the tax department in certain cases) who is dissatisfied with a first appellate order under GST can approach the GSTAT, provided they file within the allowed timelines, pay the required pre-deposit and fees, and submit the appeal through the GSTAT portal with all necessary documents. The system is designed to be fully electronic, and once you meet these conditions, your case will be registered and taken up by the Tribunal for hearing.

Q3 : What are the staggered deadlines for filing appeals to GSTAT, and how do they work?

Answer:

To prevent an overwhelming flood of appeals on day one, GSTAT has introduced a staggered filing schedule for appeals. This means the window for filing your appeal depends on the date when your first appeal (APL-01/APL-03) was originally filed (or when a revisional notice RVN-01 was issued). Essentially, older cases get to file first, and newer cases a bit later. This phased approach spreads out filings and ensures the new system can handle them smoothly.

The staggered appeal filing deadlines are as follows (as per GSTAT Order No. 1499 and the e-filing advisory):

- Category 1 – Oldest Cases:

If your first appeal was filed on or before 31st January 2022 , you can file the second appeal to GSTAT from September 24, 2025 until October 31, 2025 . For example, a first appeal filed on 15th January 2022 would fall in this category, so its GSTAT appeal window is up to 31 October 2025. (If needed, you could still file after Oct 2025 as long as it’s before the final cutoff of 30 June 2026, but it’s best to use the designated window.)

- Category 2:

If your first appeal was filed between 1st February 2022 and 28th February 2023 , your GSTAT appeal window opens on November 1, 2025 and closes on November 30, 2025 . Example: First appeal filed on 10th July 2022 → GSTAT appeal should be filed in November 2025.

- Category 3:

If your first appeal was filed between 1st March 2023 and 31st January 2024 , you can file the GSTAT appeal between December 1, 2025 and December 31, 2025 .

- Category 4:

If your first appeal was filed between 1st February 2024 and 31st May 2024 , you can file the second appeal from January 1, 2026 to January 31, 2026 .

- Category 5 – Newer Cases:

If your first appeal was filed between 1st June 2024 and 31st March 2026 , your window starts February 1, 2026 onward. Practically, this means any remaining appeals (up to those appeals decided by end of March 2026) can be filed in February 2026, March 2026, or later, but no later than June 30, 2026 . There isn’t a narrower sub-window in this category; effectively, from 1st Feb 2026 you have the freedom to file any time until the final cutoff.

A few important points about these deadlines:

- Final Cutoff of June 30, 2026:

All the above windows end no later than 30th June 2026. This date (30.06.2026) is the absolute last date to file appeals for any order passed on or before 31st March 2026. If you miss your designated window (say you forget to file in November 2025 even though your case fell in Category 2), you can still file afterward – the system will accept your appeal on any later date up to 30/06/2026 . The staggered dates are there to encourage a smooth flow, but they are not hard cutoffs until June 30, 2026. So, there is no need to panic if you miss the first window; you won’t lose your chance as long as you file by 30th June 2026.

| First Appeal Filing Date Range | Preferable GSTAT Appeal Window |

|---|---|

| On or before 31/01/2022 | 24/09/2025 – 31/10/2025 |

| 01/02/2022 – 28/02/2023 | 01/11/2025 – 30/11/2025 |

| 01/03/2023 – 31/01/2024 | 01/12/2025 – 31/12/2025 |

| 01/02/2024 – 31/05/2024 | 01/01/2026 – 31/01/2026 |

| 01/06/2024 – 31/03/2026 | From 01/02/2026 up to 30/06/2026 |

Latest by 30/06/2026 — common for all categories.

- New Appeals after April 2026:

The staggered schedule above was a special one-time relaxation since GSTAT was just set up. For any appellate orders communicated on or after 1st April 2026 , the normal rules apply – you must file the appeal within 3 months of the date the first appellate order (Form APL-04) is served to you. In other words, from April 2026 onward, GSTAT appeals will follow the regular timeline like any other tribunal (no extended deadline up to June 2026, since that extension was only for the backlog of older cases).

Always verify which category your case falls into by checking the date on your first appeal’s ARN (Application Reference Number) or CRN (Case Reference Number). The GSTAT e-filing portal will also validate the ARN date when you try to file, and it will only allow you to proceed if your slot is open as per the above schedule. The goal of this staggered approach is to give everyone adequate time to prepare and file in an orderly manner, without crashing the system. The authorities have also provided detailed guidance (manuals, videos, FAQs on the portal) to help taxpayers file appeals correctly within these timeframes.

Q4 : How do I file an appeal online through the GSTAT e-filing portal?

Answer:

Filing an appeal with GSTAT is done completely online through the official e-filing portal: https://efiling.gstat.gov.in .

The process is designed to be user-friendly and secure. Below are the steps to file your appeal via the GSTAT portal:

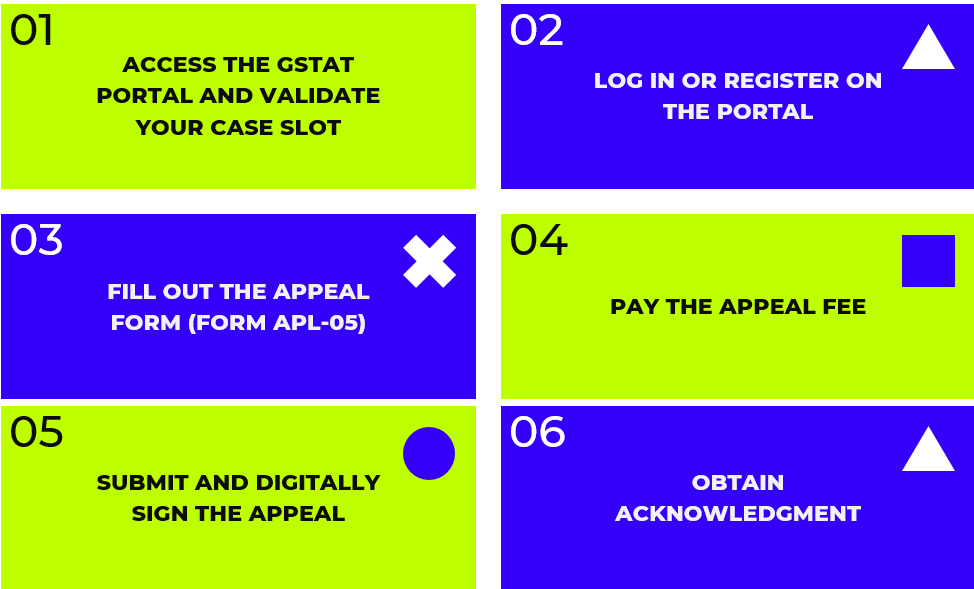

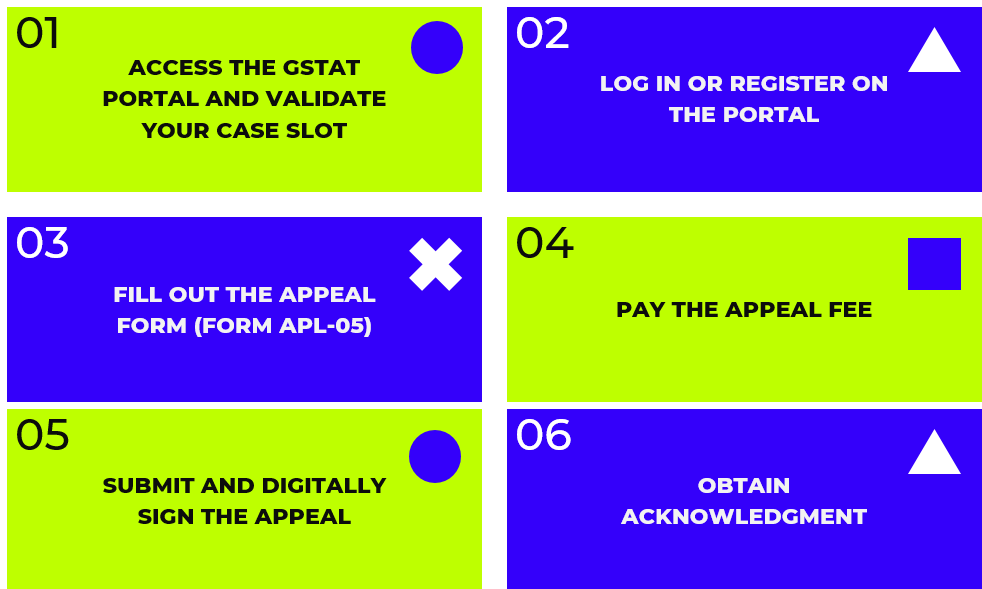

- Access the GSTAT Portal and Validate Your Case Slot:

Visit the GSTAT e-filing portal and on the home page, you’ll find a field to enter your first appeal’s ARN/CRN . Input the ARN of your original appeal (APL-01/03) or the reference of the revisional order (RVN-01). The system will check if your case is eligible for filing at this time (based on the staggered schedule).-

- If the ARN’s turn has arrived, you will get a success message and can proceed to log in or register.

- If you see a message that your slot is not currently active, that means you’re a bit early (or late) – the portal is indicating your designated window isn’t open at the moment. In that case, double-check your allowed filing dates (see the schedule above) and plan to file during that period. (Tip: There’s no need to rush if your slot isn’t open; ample time is provided up to June 2026 for older cases.)

-

- Log In or Register on the Portal:

Once your ARN is validated, the portal will prompt you to log in . You can use your existing GST credentials – taxpayers can log in with their GSTIN user ID (the same one used on the GST portal) and password, and tax officers have their own back-office IDs.

If you are a first-time user of the GSTAT system (for example, an advocate or consultant filing on behalf of a taxpayer, or a taxpayer who hasn’t used this portal before), you’ll need to complete a one-time registration process.

During registration, you will select your role (Taxpayer, Tax Officer, or Authorized Representative) and provide required details. After logging in for the first time, you’ll see a disclaimer which you must agree to, then you can access your dashboard. - Fill Out the Appeal Form (Form APL-05):

The GSTAT appeal form is an online form divided into multiple tabs. Proceed through each tab sequentially and enter the required information. The key sections to fill include:-

- Order Details:

Select the specific order (the APL-04 appellate order or RVN-01 revisional order) against which you are appealing. The system might fetch some details if available. Ensure it’s the correct order. - Basic Case Details:

Enter details like the GSTIN, order date, relevant sections, and a summary of the dispute. You can copy-paste information from your documents or use the Offline Draft Filing Excel utility provided on the portal to pre-fill these details. (Tip: The portal offers an Excel template that mirrors the appeal form – you can download it from the homepage, fill in all details offline, and then use it as reference to paste into the form. This helps avoid typos and saves time when filing online.)

- Order Details:

-

- Appellant & Respondent Info:

Verify the appellant details (your business name, address, etc.) and the respondent details (usually the GST department official who issued the order). These may be auto-filled based on your login and the order, but ensure they are correct.

- Appellant & Respondent Info:

-

- Add Authorized Representative (if any):

If you have a lawyer, CA, or other representative who will argue your case, add their details in the “Add Representative” section. (Note: The representative must be registered on the GSTAT portal for their name to appear in the dropdown. If not, they should sign up as an Authorized Representative first.) You will also need to upload a Vakalatnama or authorization letter for the representative if they weren’t already added in the system.

- Add Authorized Representative (if any):

-

- Demand Details:

Input the tax, interest, penalty amounts in dispute. The form may ask for details from the demand/order. If the system does not already have the data from your first appeal, you might need to fill the demand calculation sheet (especially if your first appeal order (APL-04) isn’t auto-available). Crucially, you must also declare the pre-deposit amount paid under Section 112(8). Ensure you have paid the required pre-deposit (e.g. an additional 10% of disputed amount, if applicable) and have the payment details handy.

- Demand Details:

-

- Upload Documents:

Attach all the mandatory and supporting documents in PDF format. This typically includes:

- Upload Documents:

-

-

- Appeal Memorandum/Grounds of Appeal – a detailed write-up of your case and arguments (often prepared separately and then uploaded).

- Copy of the Impugned Order – the first appellate order (Form GST APL-04) or revisional order you are appealing. (If the order isn’t already in the system, you must scan and upload it as PDF.)

- Supporting Documents/Evidence – any exhibits, annexures, or relevant correspondences you want the Tribunal to consider.

- Vakalatnama or Authorization Letter – if you have an authorized representative, upload the signed authority letter (scanned to PDF).

- Others – any other document required by the form or that you feel is necessary (for example, a calculation sheet for pre-deposit if not part of the form, etc.).

Make sure each file is within the size limit (currently 20 MB per file) and in PDF format. The portal will show upload buttons for the required document types.

-

-

-

- Checklist and Preview:

Once all details are filled and documents uploaded, the portal will present a final checklist to confirm everything is in order. Verify each item (the form will list items like “pre-deposit paid – Yes/No”, “copy of order uploaded – Yes/No”, etc.). This is your last chance to review. After confirming, you can preview the entire application in PDF form to double-check all entries.

- Checklist and Preview:

-

-

- Pay the Appeal Fee:

GSTAT appeals require payment of a fee (often a few thousand rupees, depending on the case). The portal provides a “Court Fee Payment” section (or tab) for this. It is recommended to complete all form filling and document uploads before making the payment. When ready:

- Choose Online Payment to be taken to the secure Bharatkosh payment gateway. You can pay using Net Banking, Credit/Debit Card, UPI, etc., just like paying any government fee. Upon successful payment, a challan or receipt will be generated by the system.

- Alternatively, if you have already paid the required fee on the Bharatkosh website directly (offline payment option), you can upload the challan/receipt number and details in this step to record the payment. The portal will then validate it.

- Ensure the payment status is “Success” and a receipt is generated. This is necessary for the appeal to be submitted. (If payment fails or is incomplete, your appeal will not be accepted.)

- Choose Online Payment to be taken to the secure Bharatkosh payment gateway. You can pay using Net Banking, Credit/Debit Card, UPI, etc., just like paying any government fee. Upon successful payment, a challan or receipt will be generated by the system.

- Submit and Digitally Sign the Appeal:

The final step is to submit the appeal and sign it electronically. The GSTAT portal supports multiple methods of digital signature for authentication :

- Digital Signature Certificate (DSC): You can use a valid Class III DSC (USB token) – either through the NIC’s DSC utility or an external utility – to sign the form. This is similar to how filings are done on the GST or MCA portals using a DSC. Make sure your system has the necessary drivers and the DSC is registered.

- Aadhaar e-Sign: If you don’t have a DSC, the portal also offers Aadhaar-based e-Sign. In this method, an OTP will be sent to the mobile number registered with your Aadhaar for authentication, and the form will be signed digitally upon OTP verification.

- Choose your preferred signing option and follow the prompts to digitally sign the appeal. Once signed and submitted, the portal will show a confirmation.

- Digital Signature Certificate (DSC): You can use a valid Class III DSC (USB token) – either through the NIC’s DSC utility or an external utility – to sign the form. This is similar to how filings are done on the GST or MCA portals using a DSC. Make sure your system has the necessary drivers and the DSC is registered.

- Obtain Acknowledgment:

After successful submission, the portal will generate a final acknowledgment with a unique Filing Number (and possibly an ARN for the appeal). This confirmation will also be sent to your registered email and via SMS to your phone. Save or print this acknowledgment for your records. You can use the filing number to track the status of your appeal on the GSTAT portal going forward.

After Filing:

Your appeal is now filed. The GSTAT registry will scrutinize it and then list it for hearing. You can track the progress of your case on the portal and you will be notified of hearing dates. Hearings may be held virtually (online) through the e-courts module of the portal, so you might get a link or login for a video hearing when your case is scheduled. Make sure to attend the hearings or have your representative attend. The portal will also allow you to download order copies and check interim updates once the Tribunal starts processing your case.

Overall, the GSTAT e-filing portal is intended to make the appeal process convenient and paperless. If you prepare your documents and information beforehand, the online form is straightforward. There are FAQs, user manuals, and even tutorial videos available on the portal to assist you at each step. With a bit of preparation, you can file your GST appeal from your office or home without needing to visit the tribunal in person, which is a big plus for business owners.

Q5 : How does GSTAT ensure fair and speedy justice for taxpayers, and how does it improve the ease of doing business?

Answer:

The establishment of the GST Appellate Tribunal is a major step toward making tax dispute resolution fair, transparent, and efficient, which in turn boosts business confidence.

Here are several ways GSTAT is designed to ensure justice is delivered swiftly and fairly, thereby improving the overall business climate:

- Swift and Timely Justice:

GSTAT has been instituted with a clear mandate that no taxpayer should face undue delays in getting justice. The Union Minister of State for Finance assured that “every taxpayer’s appeal will be heard, your rights will be protected, and there will be no delay in justice” .

This commitment to timely hearings and orders means businesses won’t be stuck in endless litigation. Quick resolution of tax disputes helps companies maintain healthy cash flow (as refunds or disputed taxes are resolved faster) and focus back on their core operations.

- Fair and Independent Forum:

The tribunal is an independent forum with a balanced bench – comprising two Judicial members and one Technical member each from Centre and State in every bench. This composition ensures that decisions are impartial, blending legal expertise with technical GST knowledge from both governments.

A strong appellate mechanism like this instills trust among taxpayers that their case will be judged on merit, free from any bias. Both small and large businesses are assured a level playing field and a chance to be heard by an expert panel, which reinforces the feeling of fairness in the system.

- Consistency and Predictability:

Before GSTAT, different states or zones might interpret GST laws differently in appeals. Now with a national tribunal, there will be more consistency in interpretation of GST regulations and predictability in outcomes . A specialized forum ruling on GST issues across India will develop a uniform jurisprudence. This predictability is crucial for businesses – when tax laws are applied consistently, companies can plan better and there are fewer surprises.

It adds credibility to the appellate process and builds investor confidence, as noted by the Revenue Secretary: GSTAT “can bring consistency in interpretation, predictability in outcomes, and credibility to the appellate process… vital for strengthening trust between taxpayers and tax administration” .

- Modern Digital Processes for Efficiency:

GSTAT is “digital-by-default” from the start – using e-filing of appeals, electronic case management, and virtual hearings. This reduces paperwork, travel, and procedural hassles for taxpayers. Cases can be filed and tracked online, and even heard via video conferencing when suitable. Such tech-driven processes make the system more efficient and transparent, leading to faster disposals. There are also time standards set for listing and resolving cases.

All these measures ensure that justice is delivered at a faster pace than traditional forums. Speedy dispute resolution directly translates to an improved ease of doing business , as businesses spend less time in courts and more time running their operations.

- Reduced Legal Costs and Burden:

With clear procedures, online guidance materials, and a focus on simplicity, GSTAT lowers the compliance burden on taxpayers fighting a case. For example, decisions are to be written in plain language without excessive jargon. The process encourages using checklists and standard formats so that taxpayers know exactly what information is needed.

This user-friendly approach means even small businesses or startups – who may not have big legal teams – can appeal their case without prohibitive effort or cost. Moreover, by addressing and clearing the backlog of GST disputes in a systematic way, GSTAT will free many businesses from long-pending issues. Timely justice also means that if a taxpayer is owed relief, they get it sooner; and if tax is owed to the government, it’s collected sooner – both aspects bring clarity and closure to all parties.

- Strengthening Taxpayer-Government Trust:

Perhaps most importantly, GSTAT’s promise of swift and fair adjudication strengthens the trust between the business community and the tax administration. It sends a message that India’s tax system is not just about tax collection, but also about protecting taxpayer rights . Investors and businesses see that there is a robust mechanism to address grievances.

As Shri Pankaj Chaudhary (MoS Finance) noted, a strong appellate mechanism assures businesses that India is “a reliable and fair market” and they won’t be caught in interminable litigations. This confidence encourages both domestic entrepreneurs and foreign investors to operate in India, knowing disputes can be resolved justly. In the long run, such trust and transparency contribute to a healthier economy and improve India’s ranking in ease of doing business indices.

Overall, GSTAT is a cornerstone reform that makes the GST regime more orderly and credible. By ensuring disputes are resolved more quickly and uniformly, it removes a significant pain point for businesses. This allows taxpayers to invest with confidence, focus on growth, and comply voluntarily, knowing that if disagreements arise, they have a fair forum to settle them. GSTAT thus helps make GST not only a “good and simple tax” but also a reliable and just system, aligning with the vision of minimum litigation and maximum governance in the tax arena.

Q6 : What if my first appeal ARN is not found on the GSTAT portal, or my filing slot is shown as inactive?

Answer:

Don’t worry – these scenarios can happen and the system has solutions for them.

Here’s what they mean and what you should do:

- ARN/CRN Not Found in System:

If the GSTAT portal tells you that it cannot find your ARN (Appeal Reference Number) or CRN when you try to validate your case, it likely means your first appeal or revision record isn’t present in the GSTN database that the Tribunal portal is using.

This situation may arise for older appeals or cases that were handled offline/manual by the appellate authority.

The solution: GSTAT has a special provision for such cases. The e-filing system will allow you to file these appeals only after December 31, 2025 . In fact, a dedicated filing window for cases with missing ARN/CRN will open on January 1, 2026 (midnight of Dec 31, 2025) and run until June 30, 2026 . So, if your ARN isn’t recognized, you will need to wait until this window opens. Use this time to prepare your documents (you will need to manually enter the details of your first appeal order and upload a copy of that order since the system can’t auto-fetch it). Once the window opens, you can register and file the appeal in the normal manner (the portal will skip the ARN validation step or have a special process for these cases). Essentially, no eligible appeal will be left out – those not traceable in the system are just deferred to the Jan–June 2026 period for filing.

Remember to file by June 30, 2026 in such cases.

- Filing Slot Inactive (Too Early or Missed Window):

If you enter your ARN and the portal says your slot or schedule is inactive, that means you are either too early (your designated filing window hasn’t started) or you possibly missed the suggested window but haven’t passed the final deadline yet. Double-check the staggered schedule (see the earlier FAQ on deadlines) to confirm when your filing is permitted. For example, if your first appeal was in November 2023, the schedule says you can file in December 2025 – if you try in October 2025, the system will give an inactive slot message because it’s not December yet.

The course of action here is to simply wait until your window opens . Mark the start date on your calendar and plan to file then. There is no penalty for not filing on the first day – the window usually is a month long. And even if that month passes, as mentioned, you can still file afterward until June 2026.

The key point is: don’t panic. The government has emphasized that more than sufficient time has been provided for all taxpayers to file their appeals within the deadlines. If you missed your initial slot (say you were busy and November 2025 passed), you can still log in later (e.g. in February or March 2026) and the portal will allow it because the final cutoff is 30th June 2026. So “inactive slot” basically means “not yet” in most cases – just follow the staggered timeline. If you believe your slot should have been active but isn’t (due to a possible technical glitch), you may reach out to the GSTAT helpdesk for assistance.

In summary, an unrecognized ARN means your case will be handled in the Jan–June 2026 batch (keep your documents ready), and an inactive slot message means you need to file during your allotted time (or afterward, but before the final deadline). The system is put in place to manage traffic, so use the schedule to your advantage. Plenty of time is given to ensure everyone who wants to appeal to GSTAT can do so comfortably. If in doubt, refer to the official advisory or contact GSTAT support – but rest assured, no genuine appellant will be left without recourse due to these technical checks.

Q7 : How GST DOST can help with GSTAT appeals and other GST compliance challenges?

Answer:

We take your case end-to-end— evaluate, prepare, file, and fight—so you don’t miss deadlines, paperwork, or strategy. Below is exactly how we help, mapped to the new GSTAT process and rules.

- Case merit & strategy (before you file)

- Quick assessment of the first-appeal/revision order (APL-04/RVN-01), limitation, chances of success, and relief strategy.

- Map your undefinedstaggered filing window so you file in the correct slot (and never beyond the final 30-Jun-2026 cutoff). We align your dates with the official schedule and ARN/CRN validation flow on the GSTAT portal

- Deadline & slot management

- We calendar your specific window (e.g., Sept–Oct 2025, Nov 2025, Dec 2025, Jan 2026, or from Feb 2026) and watch for the undefined“slot active” status the portal uses via ARN/CRN validation

- If your undefinedARN/CRN isn’t in GSTN, we queue your filing for the special window undefinedJan–Jun 2026 provided by the advisory

- Documents & drafting (done right the first time)

- Prepare a strong undefinedAppeal Memorandum (facts, grounds, reliefs), annexures, affidavits, and undefinedVakalatnama.

- Format & size-check all PDFs (≤20 MB each) per portal rules; use the undefinedoffline Excel utility to pre-stage data and eliminate typing errors during e-filing

- Portal e-filing & compliance

- undefinedE-filing only: We complete your filing on the official GSTAT portal, which is fully electronic by design —from case creation to hearing.

- Enter order details, party info, representative details, demand breakup, and upload all required PDFs, exactly as the portal tabs require

- Money side—pre-deposit & appeal fee

- Compute the undefinedpre-deposit under s.112(8) and guide payment so your appeal is admissible.

- Pay the undefinedappeal fee via the integrated undefinedBharatkosh gateway and upload challan if paid offline.

- Digital signature, submission & proof

- Execute DSC (NIC/external utility) or Aadhaar e-Sign, submit, and secure your filing number + acknowledgement (email/SMS) for audit trail and tracking.

- Execute DSC (NIC/external utility) or Aadhaar e-Sign, submit, and secure your filing number + acknowledgement (email/SMS) for audit trail and tracking.

- Hearing readiness & representation

- Prepare brief notes, case law binders, and checklists to fit GSTAT’s push for plain-language, time-bound proceedings and virtual hearings where applicable

- Appear/assist in hearings (virtual or physical), manage adjournments, and handle post-order steps (rectification/review/next remedies).

- Tracking & updates

- Ongoing cause-list monitoring, status tracking, and proactive client updates through the e-Courts workflow unveiled for GSTAT.

- Ongoing cause-list monitoring, status tracking, and proactive client updates through the e-Courts workflow unveiled for GSTAT.

- Beyond appeals—full-spectrum GST support

- SCN/ADJ defense, audits, refunds, reconciliations, and preventive compliance so you avoid disputes before they arise.

- Team training for your staff on GSTAT filing steps, including role selection, slot validation, and file standards.

Call us when:

- Your appeal window is near (or your ARN shows “slot active”).

- Your ARN/CRN isn’t found—we’ll schedule you for the Jan–Jun 2026

- You need fast, paper-tight filing and confident hearing support.

From the desk of GST DOST (Vikash Dhanania): We make GSTAT appeals predictable, punctual, and persuasive—so you protect cash flow, reduce litigation friction, and get back to business.

Conclusion:

The GST Appellate Tribunal is a significant development for taxpayers, and while it promises greater fairness and speed, it also involves new procedures to learn. This FAQ guide has hopefully answered the main questions business owners have – from what GSTAT is, who can approach it, the deadlines, the filing process, to the broader benefits it brings. Remember, you are not alone in this journey.

Experts like CA Vikash Dhanania, CA Aditya Dhanania, Adv Goutam Karmakar, Adv Sumit Jaiswal, CA Manish Jain, CA Shruti Tapadia, GST Prof. Soumen Shee etc. from GST DOST are available to assist if you need professional help. With the right knowledge and support, you can confidently navigate GSTAT and any other GST challenge that comes your way, ensuring your business remains compliant and your rights are protected.