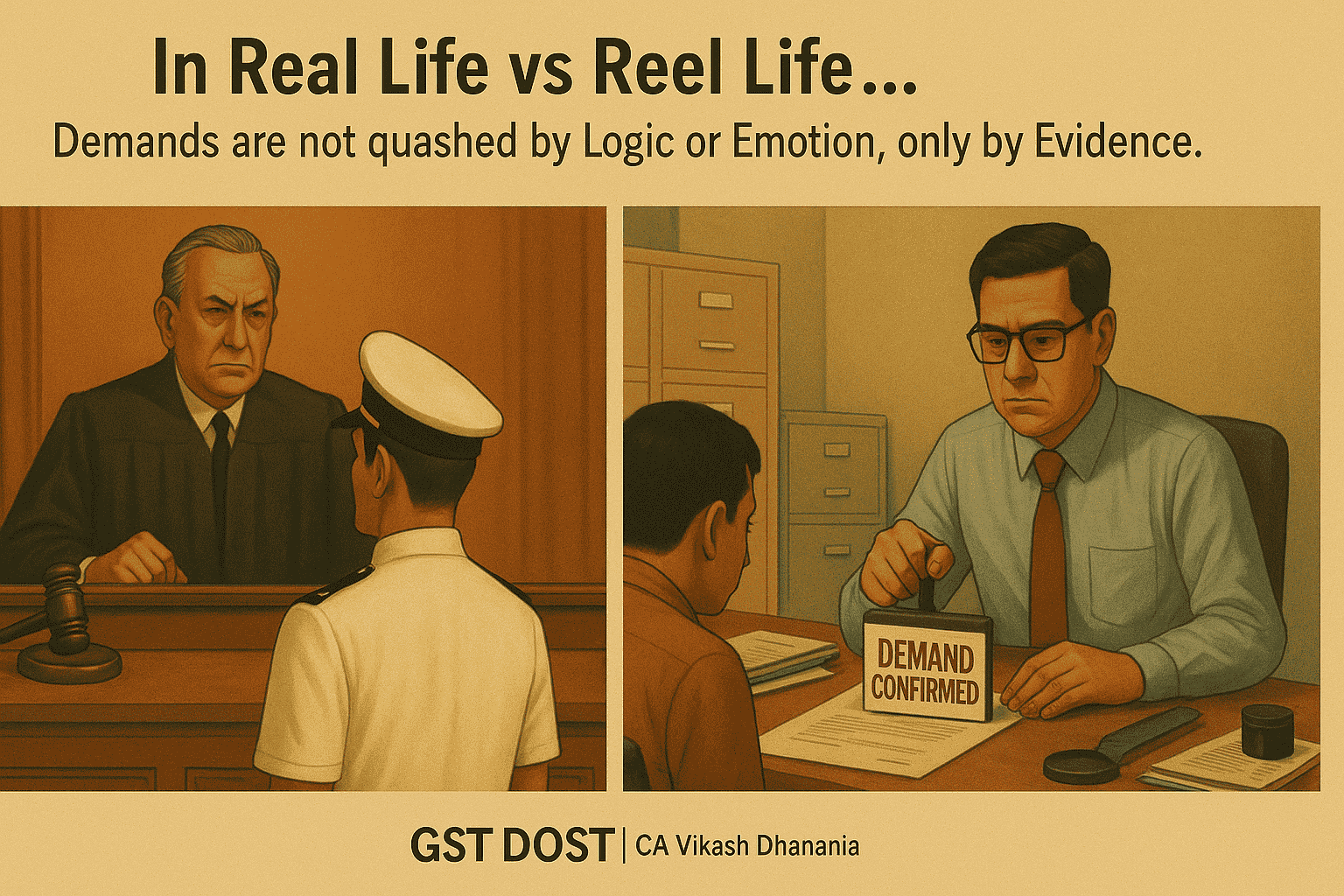

Demands are not quashed by logic or emotion but only through a combination of Evidence, Reply, and Representation.

🌟 Introduction – Life is Not Cinema

Cinema often shows us a world where the hero always wins, public sympathy and emotions can overturn judgments, and dramatic dialogues are enough to secure justice. Real life, however, works differently. Courts and Tax Authorities alike are bound not by emotions but by evidence and procedure.

To understand this difference, let us revisit one of India's most sensational criminal trials – the Commander K. M. Nanavati vs. State of Maharashtra [1962 AIR 605] – and then draw parallels with how taxpayers face GST disputes today.

💔 The Nanavati Case – Love, Betrayal, and Three Shots

In 1959, Commander K.M. Nanavati, a respected naval officer, discovered that his wife, Sylvia, was having an affair with a businessman, Prem Ahuja. Shocked and enraged, Nanavati dropped his family at a cinema, collected his service revolver, and went to confront Ahuja. After an exchange, he fired three bullets, killing Ahuja instantly. Nanavati surrendered himself to the police.

A sensational trial followed, drawing intense media attention. Public opinion largely viewed him as a "betrayed and wronged husband. The jury, swayed by public sympathy, declared him not guilty. But the Honourable Bombay High Court overturned this verdict, convicted him of murder, and highlighted the failure of jury trials to remain free from public emotion. Ultimately, this case became the turning point that led to the abolition of jury trials in India.

👉 Lesson:

Public opinion and emotions may influence people, but evidence alone decides the outcome in law.

🎥 On the Silver Screen – Rustom

Decades later, this real case was adapted into the Bollywood film Rustom (2016). Starring Akshay Kumar, the movie presented the naval Officer as a patriotic and honourable man betrayed in marriage. Courtroom scenes were filled with drama and applause, and eventually the hero was acquitted in the film.

In reality, however, Nanavati was convicted. The contrast between the reel and the real showed a vital truth: Cinema satisfies emotions; courts decide on facts and evidence.

📑 Now let us turn to the GST landscape…

Now, let us step into the life of a modern taxpayer.

Imagine you are a businessman who:

- You have purchased goods,

- The supplier's GSTIN was shown as active on the government portal,

- Payment was made through proper banking channels,

- You hold valid tax invoices, and

- The Input Tax Credit (ITC) also appears in your GSTR-2A/2B.

Suddenly, the GST department serves you a notice:

👉 "You have availed bogus ITC. Reverse the credit. Demand Confirmed."

Your natural reaction is to say:

- "What is my fault?"

- "I complied with all requirements."

- "The GST number was active on the portal."

But the department's reply will be:

👉 "We do not accept emotions. Show us evidence."

⚖️ The Formula for Success in GST: Evidence + Reply + Representation

Like the Nanavati case, the High Court relied solely on evidence; in GST matters, authorities only look at records and proof.

If you want to have a demand quashed, you must ensure the right combination of three essential elements:

- Evidence:

-

- Proof of actual receipt of goods (such as consignment note, toll tax receipts, fast tag route confirmation, weighment slip, photographs of the loading/unloading location, and a valid vehicle number corroborated by E Way Bill, etc.);

- Proof of payment through banking channels to the vendor, transporter, etc.

- Reconciliation of invoices with GST returns (GSTR-2A/2B and GSTR-3B).

- Email Communication;

- Reply:

-

- A point-by-point response to every allegation made in the notice,

- Supported by references to the relevant provisions of the CGST/SGST Acts, Rules, and applicable judicial precedents.

- Representation:

-

- Professional presentation of legally backed arguments before the Adjudicating Authority or Appellate Forum;

- Systematic production and explanation of evidence in support of the taxpayer's case.

👉 In short, Demands are quashed only through the right combination of Evidence + Reply + Representation.

🚨 Surrender or Emotional Pleas Do Not Help

Nanavati surrendered himself to the police, but he was still convicted. Similarly, appearing before the Officer in GST proceedings and merely saying, "It was not my fault, " will not save you.

The department will not be moved by sympathy. Relief comes only when you place evidence before the authority.

🙌 Reel Vs Real – The Contrast in GST

- In Reel Life: The hero is saved by emotional speeches and dramatic dialogues.

- In Real Life (GST): The taxpayer is saved only by proper compliance, documentation, and professional Representation.

The Nanavati trial and its film adaptation, Rustom, demonstrate this difference clearly. The film acquitted the Officer to satisfy popular sentiment, while the real court convicted him. Similarly, in GST, what feels "fair" emotionally does not matter unless it is backed by law and evidence.

✅ Conclusion – Why GST DOST?

The same principle applies in GST. Whether—

- Your supplier has absconded,

- Their GSTIN has later been cancelled, or

- The ITC continues to reflect on the portal —

The department will look only at whether you can produce evidence, a proper reply, and professional Representation.

👉 And this is precisely where GST DOST steps in.

Our team:

- conducts a thorough examination of the case,

- assist in compiling supporting documentary evidence,

- drafts a legally sound reply, and

- presents strong professional Representation to safeguard your interests before the authorities.

📩 What Should Be Your Next Step?

If you, too, have received a GST notice — whether it relates to ITC disallowance, bogus billing, or a demand confirmation —

👉 Do not waste time relying on emotions.

👉 Approach the matter with Evidence + Reply + Representation, together with GST DOST.

In GST, success does not come through emotion or logic alone but through a professional defence strategy.

📞 Contact GST DOST | CA Vikash Dhanania

👉 We are ready to turn every GST dispute into a victory for you.