YOU ARE HERE Home > Blogs > Reason To Believe, Not Just Suspicion

Reason To Believe, Not Just Suspicion

GST DOST's BLOG

| Ownership | Own | ||

Namaste DOST!

Today we unpack a crisp High Court ruling that every CFO and tax manager should bookmark. When can the department block your Input Tax Credit (ITC) under Rule 86A? Only when there’s a real, written “reason to believe,” not a guess, not a label.

Summary

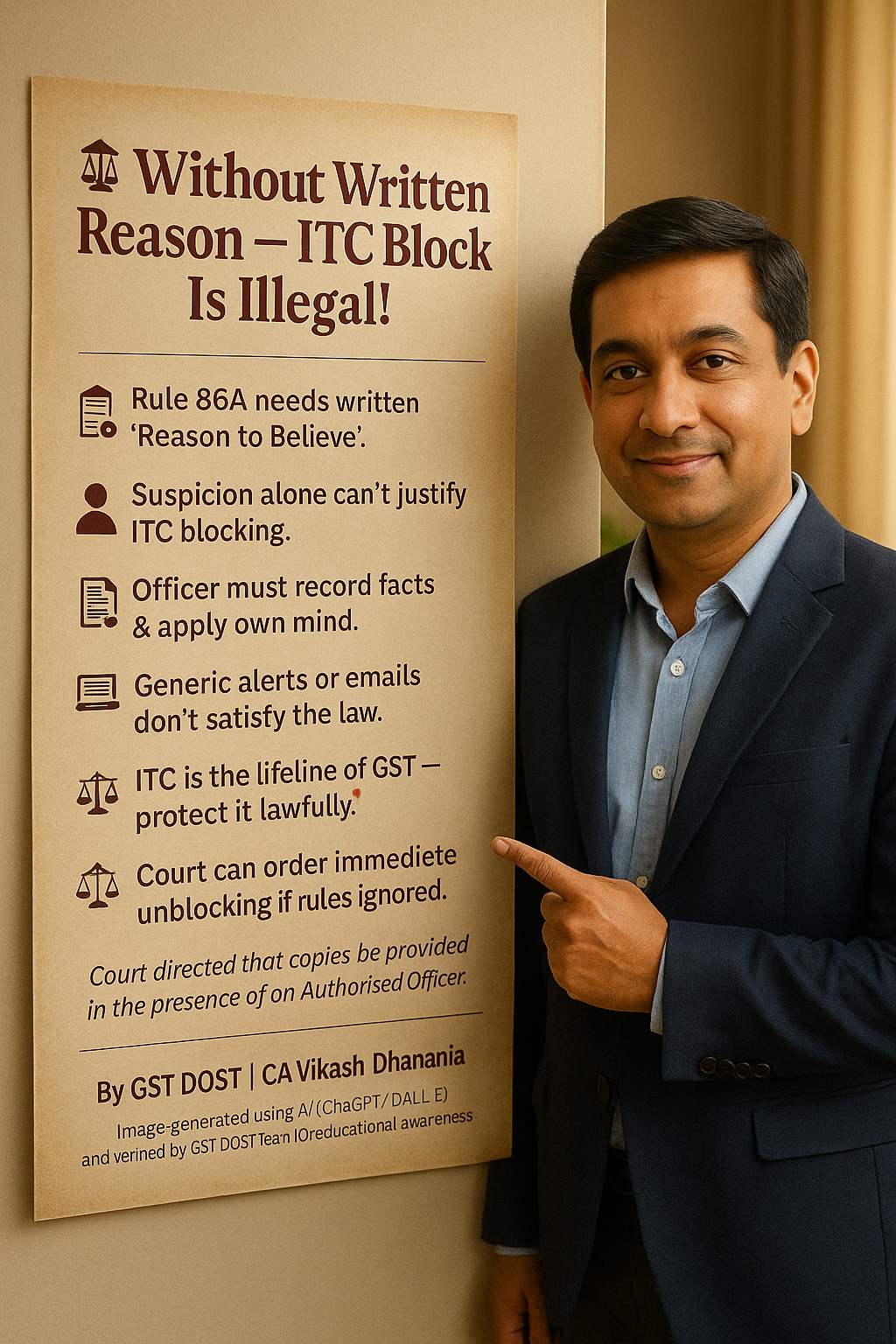

The Allahabad High Court (Oct 29, 2025) set aside the blocking of a taxpayer’s ITC that had been frozen through an email dated 24.07.2025 with the remark “Supplier found non-functioning.”

The Court held that Rule 86A requires reasons to believe to be recorded in writing, and that requirement is mandatory.

A generic DGGI alert and a one-line note do not show application of mind to the taxpayer’s transactions.

Result: the blocking action was quashed and the ITC directed to be unblocked forthwith, though the authority may proceed afresh strictly in accordance with law.

Facts of the Case

The petitioner sought unblocking of ₹13,96,220 ITC in its Electronic Credit Ledger. The blocking was communicated by GSTN via email dated 24 July 2025.

The “Reason” shown in the ledger was — “Supplier found non-functioning.”

An attachment referenced an “Alert Notice” dated 13 June 2025 from DGGI, Raipur Zonal Unit to the State GST Commissioner. The alert alleged that M/s Maa Kamakhaya Trading, Surguja had passed on fraudulent ITC without supply.

The petitioner argued that no action under Rule 86A could be taken unless the empowered officer first recorded reasons to believe in writing.

The State, on the other hand, said no prior hearing is required under Rule 86A, though the taxpayer may object by representation to the Commissioner under Rule 86A(2).

Legal Issue

Whether the department could block the petitioner’s ITC under Rule 86A based solely on a generic remark (“supplier non-functioning”) and a DGGI alert, without recording a written “reason to believe” that specifically connects the petitioner’s credit to any fraudulent transaction.

Arguments

Petitioner’s Stand:

No order or communication under Rule 86A can stand unless the officer first records written reasons to believe. Otherwise, the action is without jurisdiction and illegal.

State’s Stand:

Rule 86A does not mandate a hearing before blocking. The taxpayer may file a representation under Rule 86A(2) to object.

⚖️ High Court’s Ruling

Court: Allahabad High Court, M/s Pilcon Infrastructure Pvt. Ltd. v. State of U.P., Writ Tax No. 4654 of 2025, Judgment dated 29 October 2025.

Decision:

The Court held that no “reason to believe” was recorded in writing by the empowered officer before blocking the ITC.

Rule 86A makes this recording non-negotiable and mandatory, even if the action is ex-parte.

Therefore, the email-based blocking was set aside and the ITC directed to be unblocked forthwith, while leaving it open to the authority to proceed strictly in accordance with law in future.

Key Observations:

The Court emphasized that the statute’s requirement to record reasons “is a non-negotiable condition,” and “what constitutes ‘reason to believe’ is not a matter of speculation.”

It also reiterated that granting ITC and maintaining its chain is the soul of a successful GST regime, so mere doubt or suspicion cannot justify blocking ITC.

Supporting Precedents:

-

Commissioner of Sales Tax, U.P. v. Bhagwan Industries (P) Ltd. — “reason to believe” requires a rational basis, not pretence; sufficiency is not justiciable, but existence must be real and in good faith.

-

State of U.P. v. Aryaverth Chawal Udyog — the material cannot be arbitrary, vague, distant or irrelevant; change of opinion without new, relevant material does not create “reason to believe.”

Reasoning & Analysis

The remark “Supplier found non-functioning” did not show any application of mind to the petitioner’s transactions.

A general DGGI alert, by itself, cannot become the taxpayer-specific “reason to believe” mandated by Rule 86A(1).

The Court noted that the DGGI communication was generic and non-specific, and the investigation was ex-parte to the petitioner, with no order proving that the

petitioner’s purchases were bogus.

The Rule demands two things:

1. Material that could give rise to belief, and

2. Reasons that spring from that material, recorded in writing by the competent authority.

Both were missing.

In simple words — blocking ITC without a written, case-specific basis is like stopping an entire production line because someone heard a noise. The law expects you to find the fault, record it, and then act. That order protects the ITC value chain, which the Court rightly called the “soul of GST.”

Important Takeaways (For Business Owners)

-

Written Reasons Are Mandatory:

If your ITC is blocked, ask for the written “reason to believe” recorded by the officer. A one-line tag is not enough.

-

Generic Alerts Don’t Work:

A DGGI alert alone can’t justify blocking ITC. The officer must link it to your own transactions with supporting material.

-

Ex-Parte ≠ Free Pass:

Even if no hearing is given, officers must still write down specific, valid reasons in their records.

-

Mind The Chain:

ITC is the backbone of GST. Breaking it without fulfilling Rule 86A requirements affects the whole compliance ecosystem.

-

Know Your Right:

You can file a representation under Rule 86A(2) and, if ignored, approach the High Court citing this precedent.

Why This Matters

This verdict reminds every tax officer that Rule 86A is not a shortcut for suspicion.

It enforces accountability — if the reasons aren’t written, the ITC block won’t stand.

For businesses, it offers a strong defence and strengthens trust in the legal process.

Conclusion

What began with a single email ended with a clear message from the Court:

“Fairness is mandatory, not optional.”

If the department wants to block ITC, it must put its reasons in writing — specific, logical, and genuine.

That’s how the GST system stays balanced between compliance and confidence.

At GST DOST, we believe that lawful transparency is the best protection for every honest taxpayer.

📞 Need help with a similar case? Contact GST DOST for personalized support.

FAQ

Q: What was the dispute in this case?

A: The taxpayer’s ITC was blocked through an email stating “supplier non-functioning,” without any written “reason to believe” recorded under Rule 86A.

Q: How did the High Court rule?

A: The Allahabad High Court quashed the ITC blocking and directed immediate unblocking, while allowing the authority to act afresh per law.

Q: Does Rule 86A require a prior hearing?

A: No hearing is required before blocking, but reasons must be recorded in writing. The taxpayer can later object under Rule 86A(2).

Q: Can a generic DGGI alert justify blocking ITC?

A: No. Only taxpayer-specific, evidence-based reasons recorded by the officer can justify blocking under Rule 86A.

Q: Can ITC be blocked merely by writing “Supplier non-functioning”?

A: No. Unless the officer records a written and specific “reason to believe” supported by concrete evidence, such ITC blocking cannot legally stand.

References

-

M/s Pilcon Infrastructure Pvt. Ltd. v. State of U.P. & Another, Writ Tax No. 4654 of 2025, Allahabad High Court, Judgment dated 29 October 2025.

-

Rule 86A, U.P. GST Rules, 2017 – requires “reasons to believe” to be recorded in writing.

-

Commissioner of Sales Tax, U.P. v. Bhagwan Industries (P) Ltd., (1973) 3 SCC 265.

-

State of U.P. v. Aryaverth Chawal Udyog, (2015) 17 SCC 324.

Keywords: Rule 86A ITC blocking, Input Tax Credit unblocking, reason to believe GST.

Written by CA Vikash Dhanania | Reviewed by GST DOST Legal Research Team | Updated on 08/11/2025

“At GST DOST, we help businesses protect their lawful right to Input Tax Credit — ensuring that no officer blocks ITC without written reasons or due process.”

CBIC Notifies New Rule 14A – Quick GST Registration Option for Small Taxpayers [News]

[News]

GST Summons Is Not a Punishment — Don’t Panic Before the Law Does [Blog]

Yes, Police Can Attach Bank Accounts in GST Cases. But Only If They Follow the Law [Blog]

Gujarat HC says:“Phone calls don’t count as hearings!”Know your rights under Sec 75(4) [Video]

Know GST Rate of HSN 3926 | GST DOST [Video]

GST DOST, formerly known as My Service Tax, is a specialist GST firm led by experienced professionals — including CA, CS, MBA, and Advocates.

We are fluent in the ever-evolving GST regime and ensure accurate, timely, and actionable advice. Our strength lies not just in technical depth but in the use of AI tools and behavioural intelligence to ensure our clients feel informed, assured, and genuinely supported at every stage.

Powered by: RNJ Consultancy Services